Which Technology Trends Will Drive Future Grower Success?

January 26, 2024

How to Orchestrate an Effective S&OP Process for Growers: A Comprehensive Guide

February 9, 2024

At the end of the grower supply chain, after the product has been planned, sourced, produced, inventoried, grown, picked, packed, shipped, and invoiced is the real bottom line, getting paid.

Getting paid means accepting payments, of varying types and forms.

More growers are accepting credit card payments, and some are seeing a higher percentage of credit card transactions overall as some customers take advantage of reward credit cards and cash flow flexibility offered by some programs.

But, for the grower, it is still difficult to assess the impact of the transaction fees on financial results and for growers to decide how to apportion fees.

We will walk through a credit card fee example to help illustrate the financial impact and options a grower has to potentially improve sales and cash flow.

Sample Order Profit Analysis with Credit Card Fees

Here at Johnny Plant Nursery* our “Big Bad” credit card processor charges the following fee structure:

Copyright Advanced Grower Solutions

Here at Johnny Plant Nursery, I want to see what effect these credit card fees have on order profitability.

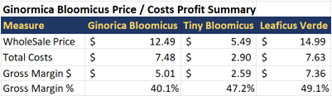

Here are some sample plants with our profitability information using our internal plant costing.

Copyright Advanced Grower Solutions

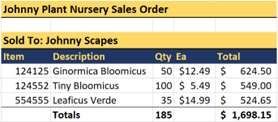

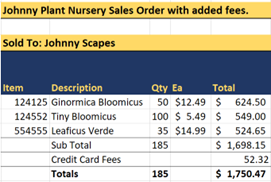

Here is an order that Johnny Plant Nursery received from our #1 customer Johnny Scapes:

Copyright Advanced Grower Solutions

Note in this case our customer picks up the order at our facility so no transportation or freight has to be considered in this example.

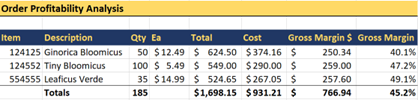

Let’s analyze this order from our costing profitability analysis perspective based on our internal item costing and see how we did on a pure cash basis:

Copyright Advanced Grower Solutions

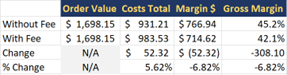

On a cash basis, we ended up with a 45.2% gross margin on this order.

Now let’s look and see how the credit card fees impact the financial results of this order.

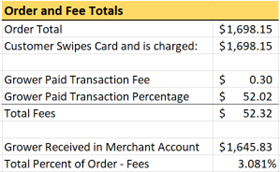

For this order, with the above credit card fee parameters, the total fees look like this:

Copyright Advanced Grower Solutions

For this order, the credit card fees amounted to 3.081% of the order total coming in at $52.32 for a $1,698.15 order total. So, the Johnny Plant Nursery bank account received $1,645.83 and the credit card processor and associates got $52.32.

Essentially in this situation, the grower paid $52.32 for the convenience of the customer to pay with a credit card.

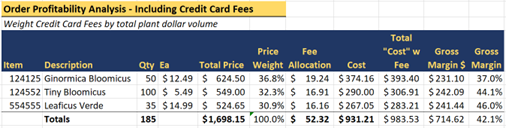

How do these credit card fees affect our order profitability?

Copyright Advanced Grower Solutions

For this order profitability analysis, we chose to allocate the credit card fees per item based on the total item price as a percentage of the total order price. See the “Price Weight” column in the table above. We are assigning that as the item weight of the order. We then allocated that percentage of the total credit card fees to that line item and presented it as the column “Total Cost w Fee” – that is the adjusted cost of the item including fee allocation.

For this order when allowing the payment by card the order based weighted gross margin goes from 45.2% to 42.1%***. This is a 6.82% reduction in our margin (-308 basis points). Adding the credit card fees increases our item costs by 5.62% over our standing cost baseline.

The table below compares the impact of the fees to the cash basis.

Copyright Advanced Grower Solutions

Reality of Payments

In today’s world electronic payments and credit cards dominate many areas of commerce.

However, in our industry, outside of the independent retail garden centers, electronic payments are still nascent for some wholesale and re-wholesale growers.

For our growers who sell to big box retailers, those payments are direct bank to bank.

For our growers that sell to a mix of landscapers, other organizations, garden centers, and re-wholesalers they can end up taking a mix of payment types to keep their customers happy.

Further, many of the customers of these growers are utilizing reward and cash back credit cards to gain a desired benefit while utilizing the cash flow tools that these cards offer to benefit their business. Thus, more and more growers are beginning to allow credit card payments. Some growers have customers who must have a card on file or must pre-pay due to collection issues in the past.

Finally, in recent years we (and many others) have directly experienced delivery issues with paper mail and paper checks which still dominate our wholesale growers’ payments who offer terms to their customers. The delay or loss of a paper check interrupts cash flow, and creates a stressful situation between grower and customer and causes rework on the part of back-office staff. This uncertainty can also pressure growers to migrate from paper checks to forms of electronic payment.

What Can Growers Do?

When thinking about credit card fees and their impact on the grower’s business a grower has four basic options.

- Don’t take credit cards and only take cash, checks, or other liquid payments.

Some growers opt for this as a way of simplifying their operation.

But, in today’s world, I believe this does present a barrier for some customers and, as the payments landscape evolves, I believe it will become an increasing barrier for some customer types.

- Take credit cards and pass on the fee to the customer at the time of purchase

In this scenario, the grower would tack on the $52.32 in credit card fees to the total order price at the point of purchase.

Copyright Advanced Grower Solutions

In this case, the customer sees and directly pays for the fee for using the credit card.

This practice is used by some growers. If a grower chooses to do this, it must be clear in the terms that this will happen if the customer uses a credit card for their payment.

If the customer has in their mind the total price of the items and then at the very last minute finds out these extra fees will increase their total order amount it can make for some tense interactions.

A further risk is you reveal your credit card fees and if your competitor down the road uses a less expensive processor then even with equivalent product pricing they end up with lower prices.

- Take credit cards and markup prices to account for the fees

This tactic would affect all prices for the grower when they decide to start accepting credit card payments. However, it eliminates any discussion or tension at the point of payment that can be induced by having the customer pay fees explicitly.

The advantage of this is that you have the same price, regardless of payment method, you recoup transaction costs for credit cards, and eliminate the occasional tense customer interaction for those who feel surprised at purchase. The downside is that prices must increase, and some competitive market areas may give growers pause at raising prices.

In our example, the credit card fees ended up being 3.081% of the order total. The table below shows the variance of the percentage of an order on the credit card fees for our scenario here at Johnny Plant Nursery.

Copyright Advanced Grower Solutions

In our case, we will use a margin value of 3.081% for determining markup. In this scenario, we need to raise our prices by just over 6% **** to fully restore our margin for credit card purchase of this order.

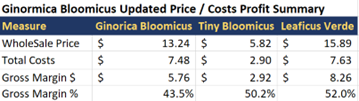

So, let’s apply that markup to our prices and see what happens to our order profitability.

Copyright Advanced Grower Solutions

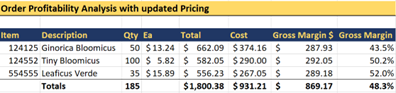

Now, with that updated pricing, let’s look at the order profitability on a cash basis.

Copyright Advanced Grower Solutions

The pricing change increased our cash basis gross margin to 48.3% from 45.2%. Now let’s look at the profitability analysis with the credit card transaction.

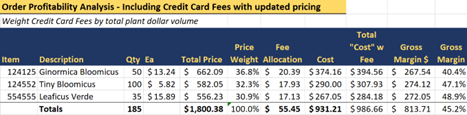

Copyright Advanced Grower Solutions

With the new pricing and the credit card fee structure, we are back to the margin we had before but for credit card purchases.

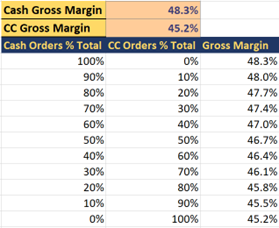

In this case, if the grower has some percentage of orders that are cash, and the remaining are credit card orders the following table shows the weighted gross margin that could be achieved in this scenario.

Copyright Advanced Grower Solutions

- Combination of lower markup prices and pass along to account for the fees

Finally, a grower could utilize a combined strategy.

They could raise prices a smaller amount and pass on a portion of the fees to credit card users on a standard flat fee or percentage basis. This is what I call the ‘share the pain’ scenario where the customer pays some (explicitly) and the grower pays some.

My Take

As the ubiquity of credit cards spills into our industry, my recommendation to growers is to utilize a credit card processing partner that can help optimize the transaction costs and bake the fees into your pricing accounting for transaction fees.

As we have seen in this example, depending on your ratio of cash to credit card orders, you can bump your overall weighted margin and allow your customers the transparent flexibility to pay in the manner best for them.

Bottom Line

Electronic and specifically credit card payments are increasing in frequency in our industry.

Growers must examine their business, cost structure, and customer makeup to decide if they will take credit cards and if so, how to structure pricing and or pass along fees.

To help growers navigate these decisions AGS has teamed up with Propelr, a leading payments processor who, with their platform can help optimize grower transaction fees for credit cards and online payments.

If you need help with the financial analysis or pricing analysis our consultants have the data skills and experience to help you see a clearer picture of scenario impacts like this.

Contact us today to find out more about how our consultants can help you see your business more clearly or how GrowerPay and our partner Propelr can help you with credit card payments.

Notes

*Johnny Plant Nursery (and Johnny Scapes) are fictional companies in the fictional town of Redstone, TX, and used to illustrate real grower financial situations we encounter when consulting and helping growers with consulting, software, and system needs.

** https://quickbooks.intuit.com/payments/payment-rates/ I used the average of the big three credit card processors for invoice-based transactions (card not present). Card present transactions are typically lower but growers who offer terms end up with the invoice base method many times since the invoices can be paid online (not present). Growers who have retail operations with card present terminals can benefit from lower fees for those transactions.

*** Most grower financial income or P&L statement show bank fees below the gross margin line as part of ‘expenses section. For this case, to illustrate the direct impact of the fees we are adding them to item ‘costs’ in order to see the order-by-order impact of the additional fees even though in most cases the fees would not be part of a true item cost or traditional nursery/greenhouse gross margin calculations.

**** Normally in item costing all internal costs such as raw materials, labor, and other allocated overhead costs are marked up as a summed unit once to achieve a desired margin. Doing the markup calculations outside that empirically as we have done here results in a higher value than the standard markup equations would generate but the empirical method gets us full restoration of the original weighted gross margin prior to include fees which was our goal for this exercise.